GST Reconciliation: The Complete Guide to GSTR-1, GSTR-2B & GSTR-3B Reconciliation

Keeping GST records accurate is one of the most important responsibilities for every registered business. Every invoice issued, every purchase made, and every tax payment reported should match the information submitted through GST returns. Even a small mismatch can result in denied Input Tax Credit (ITC), notices from tax authorities, penalties, or unnecessary compliance work.

This is where GST reconciliation becomes an essential business process.

GST reconciliation is the practice of comparing your accounting records with GST returns and supplier data to ensure that every transaction is accurate and complete. Businesses that reconcile their GST data regularly can identify discrepancies early, recover eligible tax credits, and file returns with greater confidence.

Whether you are a small business owner, accountant, finance manager, or tax consultant, understanding GST reconciliation can significantly improve compliance while reducing manual effort.

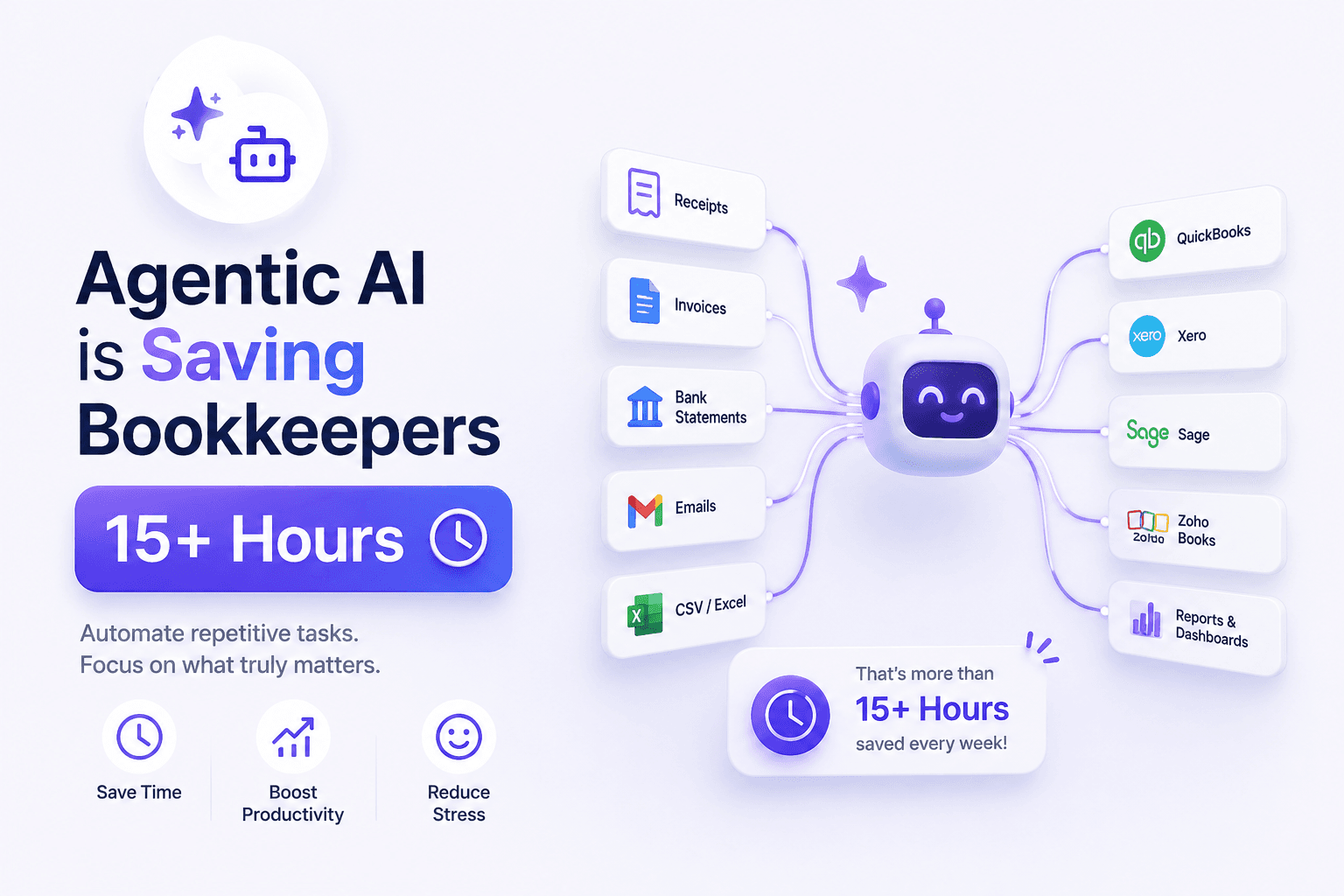

Modern businesses also deal with invoices received in multiple formats, including PDFs, scanned documents, emails, and images. Extracting invoice information manually is time-consuming and increases the likelihood of errors. Intelligent document processing solutions such as BillsDeck help automate invoice data extraction, making GST reconciliation faster and more reliable.

Table of Contents

- What is GST Reconciliation?

- Why GST Reconciliation is Important

- Types of GST Reconciliation

- Understanding GST Returns Used in Reconciliation

- GST Reconciliation Process

- GSTR-1 Reconciliation

- GSTR-2B Reconciliation

- GSTR-3B Reconciliation

- Purchase Reconciliation

- Sales Reconciliation

- Common GST Mismatches

- GST Reconciliation Example

- Best Practices

- Automating GST Reconciliation

- GST Reconciliation Checklist

- Frequently Asked Questions

- Conclusion

What is GST Reconciliation?

GST reconciliation is the process of comparing financial records maintained by a business with the information available in GST returns and supplier filings.

The objective is to ensure that:

- Every sales invoice is correctly reported.

- Every purchase invoice is recorded.

- GST paid matches GST collected.

- Input Tax Credit claimed is eligible.

- Supplier invoices appear correctly in GSTR-2B.

- Tax liabilities reported in GSTR-3B are accurate.

Instead of relying solely on accounting software, reconciliation verifies that the information submitted to the GST portal is consistent with internal records.

A reconciliation process typically compares information across multiple sources:

| Source | Compared Against | Purpose |

|---|---|---|

| Sales Register | GSTR-1 | Verify outward supplies |

| Purchase Register | GSTR-2B | Verify eligible ITC |

| General Ledger | GSTR-3B | Verify tax liabilities |

| Bank Statements | Accounting Records | Verify payments |

| Supplier Invoices | Purchase Register | Verify vendor transactions |

| Customer Invoices | Sales Register | Verify sales reporting |

The reconciliation process helps businesses identify:

- Missing invoices

- Duplicate invoices

- Incorrect GSTIN

- Wrong taxable values

- Wrong GST rates

- Missing Input Tax Credit

- Supplier filing errors

Why GST Reconciliation is Important

Many businesses assume that filing GST returns completes their compliance responsibilities. In reality, filing returns without reconciliation can create financial and compliance risks.

Regular reconciliation helps businesses maintain accurate financial records while ensuring compliance with GST regulations.

1. Prevents Loss of Input Tax Credit

Input Tax Credit is available only when supplier invoices are correctly reported.

Suppose your business receives 500 supplier invoices every month. If even 20 invoices are missing from supplier returns, your eligible ITC may be affected.

Regular reconciliation helps identify:

- Missing supplier invoices

- Incorrect invoice values

- Duplicate reporting

- Supplier filing delays

This allows businesses to follow up with vendors before filing returns.

2. Improves GST Compliance

Reconciliation ensures that filed returns accurately reflect business transactions.

Benefits include:

- Accurate tax liability

- Correct tax payments

- Reduced filing errors

- Better audit readiness

Businesses with strong reconciliation practices generally experience fewer compliance issues.

3. Detects Errors Early

Errors become increasingly difficult to correct after multiple filing periods.

Examples include:

- Wrong invoice numbers

- Incorrect GST rates

- Wrong HSN codes

- Incorrect taxable value

- Missing invoices

Finding these issues early reduces correction efforts.

4. Reduces Department Notices

One of the most common reasons businesses receive GST notices is mismatched return information.

Regular reconciliation minimizes differences between:

- Accounting records

- GST returns

- Supplier filings

This significantly lowers compliance risks.

5. Supports Accurate Financial Reporting

GST affects:

- Revenue

- Expenses

- Liabilities

- Assets

- Cash flow

Reconciling GST data improves the accuracy of financial statements and management reports.

Types of GST Reconciliation

GST reconciliation is not a single activity. Businesses typically perform several reconciliation processes throughout each reporting period.

Sales Reconciliation

Sales reconciliation compares:

- Sales register

- Tax invoices

- Credit notes

- Debit notes

- GSTR-1

Objectives include:

- Verify taxable sales

- Verify GST amounts

- Identify missing invoices

- Ensure accurate outward supply reporting

Purchase Reconciliation

Purchase reconciliation compares:

- Purchase register

- Vendor invoices

- GSTR-2B

- ITC claimed

The goal is to ensure that:

- Every supplier invoice exists.

- Eligible ITC is available.

- Vendors have uploaded invoices correctly.

- Duplicate invoices are eliminated.

GSTR-1 Reconciliation

This reconciliation validates outward supplies reported in GSTR-1 against accounting records.

Businesses compare:

- Invoice numbers

- Customer GSTIN

- Taxable value

- GST amount

- Invoice date

GSTR-2B Reconciliation

GSTR-2B is the primary document used to determine eligible Input Tax Credit.

Businesses compare:

- Purchase invoices

- Supplier returns

- Eligible ITC

- Blocked credits

- Pending invoices

This reconciliation is generally performed every month before filing GSTR-3B.

GSTR-3B Reconciliation

GSTR-3B reconciliation verifies:

- Output GST liability

- ITC claimed

- Net tax payable

- Tax payments

- Ledger balances

It ensures that taxes paid match business records.

Vendor Reconciliation

Vendor reconciliation focuses specifically on supplier compliance.

Businesses verify:

- Supplier GSTIN

- Invoice uploads

- Invoice values

- Filing status

- ITC eligibility

Suppliers that repeatedly fail to upload invoices can be identified and followed up promptly.

Annual GST Reconciliation

Although monthly reconciliation is recommended, businesses also perform annual reconciliation to verify the complete financial year.

Annual reconciliation includes:

- Annual sales

- Annual purchases

- ITC summary

- GST liability

- Ledger balances

- Financial statements

This helps prepare businesses for audits and year-end financial reporting.

Understanding GST Returns Used in Reconciliation

GST reconciliation involves comparing multiple GST returns, each serving a different purpose.

GSTR-1

GSTR-1 contains details of all outward supplies made during the reporting period.

It includes:

- B2B invoices

- B2C invoices

- Credit notes

- Debit notes

- Export invoices

- Advances received

The information submitted in GSTR-1 becomes visible to customers for claiming Input Tax Credit.

GSTR-2B

GSTR-2B is a static statement generated automatically based on supplier filings.

It provides:

- Eligible ITC

- Ineligible ITC

- Imports

- ISD credits

- Reverse charge transactions

Businesses should compare every purchase invoice against GSTR-2B before claiming Input Tax Credit.

GSTR-3B

GSTR-3B is the monthly summary return used to declare:

- Outward tax liability

- Eligible ITC

- Tax payable

- Tax paid

Errors in GSTR-3B directly affect tax payments, making reconciliation essential before filing.

Challenges Businesses Face During GST Reconciliation

Although the reconciliation process appears straightforward, businesses often encounter practical challenges due to the volume and complexity of transaction data.

Some of the most common issues include:

- Thousands of invoices received each month from multiple vendors.

- Supplier invoices arriving in PDF, scanned, paper, and email formats.

- Manual data entry errors during invoice recording.

- Delayed supplier filings affecting GSTR-2B.

- Duplicate invoices in accounting systems.

- Incorrect GSTINs or invoice numbers.

- Frequent amendments and credit notes.

- Mismatched taxable values or GST rates.

- Difficulty reconciling transactions across multiple branches.

- Time-consuming manual comparison between spreadsheets and GST returns.

As organizations grow, these challenges multiply, making manual reconciliation increasingly difficult. Automating invoice capture and validation before reconciliation can significantly reduce these issues by ensuring consistent, accurate data enters the accounting system from the beginning.

GST Reconciliation Process: Step-by-Step Guide

A structured GST reconciliation process helps businesses identify discrepancies before returns are filed. Rather than waiting until the filing deadline, businesses should reconcile transactions regularly throughout the month.

The following workflow is suitable for businesses of all sizes.

Step 1: Collect All Transaction Data

Begin by gathering financial data from every source used during the reporting period.

This typically includes:

- Sales register

- Purchase register

- Tax invoices

- Credit notes

- Debit notes

- Vendor bills

- Accounting software reports

- Bank statements

- GST returns

- E-way bill reports (where applicable)

Ensure all transactions belong to the same tax period before starting reconciliation.

Step 2: Validate Invoice Data

Before comparing invoices with GST returns, verify that each invoice contains mandatory details.

Check for:

| Validation | Description |

|---|---|

| Invoice Number | Unique and correctly formatted |

| Invoice Date | Falls within the reporting period |

| Supplier GSTIN | Valid GST registration |

| Customer GSTIN | Correct for B2B invoices |

| HSN/SAC Code | Applicable classification |

| Taxable Value | Matches accounting records |

| GST Rate | Correct CGST, SGST, IGST |

| Tax Amount | Calculated correctly |

| Invoice Status | Original, amended, cancelled or credit note |

Incorrect invoice information often causes reconciliation failures.

Step 3: Compare Purchase Register with Supplier Data

Next, compare your purchase register against invoices uploaded by suppliers.

Review:

- Missing invoices

- Duplicate invoices

- Incorrect GSTIN

- Wrong invoice number

- Wrong taxable value

- Incorrect tax amount

Invoices that do not appear in supplier returns should be investigated before claiming ITC.

Step 4: Compare Sales Register with GSTR-1

Every outward invoice recorded in your accounting system should appear in GSTR-1.

Verify:

- Invoice number

- Customer GSTIN

- Invoice date

- Taxable value

- GST amount

- Place of supply

Missing invoices may result in under-reporting of tax liability.

Step 5: Verify Input Tax Credit

Once supplier invoices have been matched, calculate eligible ITC.

Separate invoices into categories:

- Fully eligible

- Partially eligible

- Ineligible

- Under reverse charge

- Pending supplier filing

This helps ensure only valid credits are claimed.

Step 6: Reconcile GSTR-3B

Before filing GSTR-3B, compare:

- Output GST

- ITC available

- ITC claimed

- Net GST payable

- Cash ledger

- Electronic credit ledger

Any differences should be investigated before submission.

Step 7: Investigate Exceptions

Not every mismatch indicates an error.

Common reasons include:

- Supplier has not filed returns.

- Supplier filed with incorrect invoice details.

- Invoice entered twice.

- Credit note not recorded.

- Wrong GST rate applied.

- Amendment pending.

Each exception should be documented with corrective action.

Step 8: File Correct Returns

After resolving discrepancies:

- Update accounting records.

- Correct invoice errors.

- Recalculate GST.

- Verify totals.

- File returns.

Maintaining reconciliation reports also helps during audits.

GSTR-1 Reconciliation

GSTR-1 contains details of all outward supplies made during the tax period. Reconciling it ensures that sales reported to the GST portal match the organization's accounting records.

What Should Be Compared?

Businesses should compare the following fields:

| Accounting Record | GSTR-1 |

|---|---|

| Invoice Number | Invoice Number |

| Invoice Date | Invoice Date |

| Customer GSTIN | GSTIN |

| Taxable Value | Taxable Value |

| GST Rate | Tax Rate |

| CGST | CGST |

| SGST | SGST |

| IGST | IGST |

| Invoice Status | Filing Status |

Common GSTR-1 Mismatches

Missing Sales Invoice

An invoice exists in the ERP but is absent from GSTR-1.

Possible causes:

- Data entry omission

- Invoice deleted accidentally

- Incorrect reporting period

Wrong GSTIN

An incorrect customer GSTIN can prevent the customer from claiming Input Tax Credit.

Businesses should verify GSTINs before filing.

Incorrect Taxable Value

The taxable value in GSTR-1 differs from accounting records.

Possible reasons include:

- Manual adjustments

- Discount errors

- Incorrect taxable calculations

Duplicate Invoice

The same invoice appears multiple times.

Duplicate reporting may increase tax liability unnecessarily.

Wrong Place of Supply

Incorrect place of supply affects whether CGST/SGST or IGST applies.

This error is common in interstate transactions.

Example of GSTR-1 Reconciliation

| Invoice | Sales Register | GSTR-1 | Status |

|---|---|---|---|

| INV-101 | ₹50,000 | ₹50,000 | Matched |

| INV-102 | ₹20,000 | Missing | Investigate |

| INV-103 | ₹75,000 | ₹70,000 | Taxable value mismatch |

| INV-104 | ₹15,000 | Duplicate | Remove duplicate |

Only after resolving these discrepancies should the return be finalized.

GSTR-2B Reconciliation

GSTR-2B is one of the most important statements for claiming Input Tax Credit.

It provides a consolidated view of invoices uploaded by suppliers.

Businesses should reconcile GSTR-2B every month before filing GSTR-3B.

Information Available in GSTR-2B

GSTR-2B includes:

- B2B invoices

- Credit notes

- Debit notes

- ISD credits

- Import of goods

- Import of services

- Reverse charge transactions

- Eligible ITC

- Ineligible ITC

Why GSTR-2B Reconciliation Matters

Reconciling GSTR-2B helps businesses:

- Claim only eligible ITC

- Identify supplier filing delays

- Detect duplicate invoices

- Avoid excess ITC claims

- Reduce GST notices

GSTR-2B Reconciliation Workflow

- Download GSTR-2B.

- Export purchase register.

- Standardize invoice formats.

- Match invoice numbers.

- Compare supplier GSTIN.

- Verify invoice dates.

- Compare taxable values.

- Compare GST amounts.

- Review unmatched invoices.

- Contact suppliers if required.

Invoice Matching Criteria

A reconciliation tool generally matches invoices using:

- GSTIN

- Invoice Number

- Invoice Date

- Invoice Value

- Taxable Amount

- GST Amount

If all fields match, the invoice is considered reconciled.

Types of GSTR-2B Mismatches

Invoice Missing in GSTR-2B

Possible reasons:

- Supplier has not filed GSTR-1.

- Supplier uploaded incorrect GSTIN.

- Wrong reporting month.

Tax Difference

The GST amount differs from the purchase register.

Example:

| Purchase Register | GSTR-2B |

|---|---|

| GST ₹9,000 | GST ₹8,100 |

The invoice should be reviewed before claiming credit.

Invoice Number Difference

Small formatting differences can prevent automatic matching.

Example:

Accounting:

INV10025

Supplier:

INV/10025

Many reconciliation solutions include fuzzy matching to identify such cases.

Duplicate Supplier Invoice

Duplicate uploads may occur due to repeated imports.

These should be removed before claiming ITC.

Supplier GSTIN Error

Incorrect GSTIN results in unmatched invoices.

Businesses should request corrected filings from suppliers.

Best Practices for GSTR-2B Reconciliation

Successful organizations typically follow these practices:

- Reconcile every month.

- Avoid waiting until year-end.

- Follow up promptly with suppliers.

- Maintain vendor compliance reports.

- Archive reconciliation reports.

- Use automated invoice matching wherever possible.

- Validate GSTINs before recording invoices.

- Monitor high-value invoices separately.

Purchase Reconciliation

Purchase reconciliation compares procurement records with supplier invoices and GST returns.

The objective is to ensure that every purchase recorded by the business is supported by a valid tax invoice and reflected in GSTR-2B.

Purchase Reconciliation Workflow

Purchase Order

↓

Goods Receipt

↓

Supplier Invoice

↓

Invoice Verification

↓

Accounting Entry

↓

GST Matching

↓

ITC Validation

↓

GSTR-2B Reconciliation

This workflow ensures procurement, accounting, and GST reporting remain aligned.

Information Compared During Purchase Reconciliation

| Purchase Register | Supplier Invoice |

|---|---|

| Vendor Name | Vendor Name |

| GSTIN | GSTIN |

| Invoice Number | Invoice Number |

| Invoice Date | Invoice Date |

| Item Description | Item Description |

| Taxable Value | Taxable Value |

| GST Rate | GST Rate |

| GST Amount | GST Amount |

| Total Invoice Value | Total Value |

Common Purchase Reconciliation Issues

Businesses frequently encounter:

- Missing vendor invoices

- Duplicate invoice entries

- Wrong GST classification

- Incorrect taxable value

- Delayed supplier filings

- Incorrect invoice dates

- Manual entry mistakes

- Vendor GSTIN errors

- Unrecorded credit notes

- Purchase returns not reflected

Detecting these issues early prevents incorrect ITC claims and improves the accuracy of financial records.

Sales Reconciliation

Sales reconciliation ensures that every taxable sale recorded in your accounting system is accurately reflected in GST returns. It verifies that the revenue recognized in your books matches the outward supplies reported to the GST portal.

An effective sales reconciliation process reduces the risk of under-reporting tax, duplicate invoices, and customer disputes related to Input Tax Credit (ITC).

Objectives of Sales Reconciliation

The primary objectives include:

- Verify all sales invoices have been reported.

- Confirm GST has been calculated correctly.

- Match invoice values with accounting records.

- Identify duplicate or cancelled invoices.

- Ensure credit and debit notes are properly adjusted.

- Detect reporting errors before filing GST returns.

Regular reconciliation also helps finance teams maintain accurate revenue recognition and simplifies statutory audits.

Sales Reconciliation Workflow

Customer Order

↓

Sales Invoice

↓

Accounting Entry

↓

GST Calculation

↓

Sales Register

↓

GSTR-1 Preparation

↓

Reconciliation

↓

GST Filing

Each stage should be validated before moving to the next to avoid cascading errors.

Information to Compare

| Sales Register | GST Return |

|---|---|

| Invoice Number | Invoice Number |

| Invoice Date | Invoice Date |

| Customer GSTIN | GSTIN |

| Taxable Value | Taxable Value |

| CGST | CGST |

| SGST | SGST |

| IGST | IGST |

| Place of Supply | Place of Supply |

| Total Invoice Value | Total Invoice Value |

Common Sales Reconciliation Errors

Missing Invoice

An invoice exists in the accounting software but was not included in GSTR-1.

Impact

- Under-reported turnover

- Lower tax liability reported

- Possible GST notices

Duplicate Invoice

The same invoice appears multiple times.

Impact

- Higher tax liability

- Incorrect revenue reporting

Wrong GST Rate

Incorrect tax percentages may have been applied.

For example:

| Item | Correct GST | Applied GST |

|---|---|---|

| Office Furniture | 18% | 12% |

This results in an incorrect tax liability and requires correction.

Incorrect Place of Supply

A transaction may have been treated as intra-state instead of inter-state.

This affects whether:

- CGST + SGST applies, or

- IGST applies.

Credit Notes Not Adjusted

Credit notes issued after returns are filed must also be reconciled.

Failure to account for them can result in overstated revenue and GST liability.

Common GST Reconciliation Mismatches

Every reconciliation exercise uncovers discrepancies. Understanding the most common mismatches helps businesses resolve issues quickly.

1. Missing Supplier Invoice

The purchase register contains an invoice, but it does not appear in GSTR-2B.

Possible Causes

- Supplier has not filed GSTR-1.

- Invoice uploaded in the wrong month.

- Incorrect GSTIN used.

- Filing errors by the supplier.

Resolution

- Contact the supplier.

- Request correction or timely filing.

- Claim ITC only after the invoice is reflected, subject to applicable GST provisions.

2. Missing Sales Invoice

A sales invoice exists internally but is absent from GSTR-1.

Possible Causes

- Manual omission

- Incorrect export from ERP

- Filing oversight

Resolution

- Update GSTR-1 through amendment, if applicable.

- Strengthen invoice reporting controls.

3. Invoice Number Mismatch

Example:

Accounting:

INV-4589

Supplier Return:

INV4589

Although both refer to the same invoice, strict matching systems may flag them as different.

Recommendation

Adopt consistent invoice numbering standards across all systems.

4. GST Amount Difference

Example:

| Purchase Register | Supplier Return |

|---|---|

| ₹18,000 | ₹17,820 |

Possible reasons:

- Discount applied differently

- Rounding differences

- Incorrect GST rate

- Manual calculation errors

5. Duplicate Invoice

Duplicate invoices can occur because of:

- Multiple imports

- Duplicate ERP entries

- Supplier upload errors

Duplicate invoices should be removed before claiming ITC.

6. Incorrect GSTIN

An incorrect GSTIN prevents proper invoice matching.

Businesses should validate GSTINs while onboarding vendors and customers to reduce such issues.

7. Credit Note Missing

If a supplier issues a credit note that is not recorded, purchase values and ITC may be overstated.

8. Debit Note Missing

Debit notes increase taxable value. Missing them can result in understated GST liability.

9. Wrong Tax Period

Invoices posted in different reporting periods frequently create temporary mismatches.

Maintaining proper accounting cut-off procedures minimizes these timing differences.

GST Reconciliation Example

Consider the following scenario.

ABC Traders has completed its monthly reconciliation.

Purchase Register

| Invoice | Vendor | GST | Status |

|---|---|---|---|

| INV101 | Vendor A | ₹9,000 | Present |

| INV102 | Vendor B | ₹18,000 | Missing |

| INV103 | Vendor C | ₹5,400 | Present |

| INV104 | Vendor D | ₹12,600 | Duplicate |

GSTR-2B

| Invoice | GST | Status |

|---|---|---|

| INV101 | ₹9,000 | Match |

| INV103 | ₹5,400 | Match |

| INV104 | ₹12,600 | Duplicate |

| INV105 | ₹4,500 | Unknown Invoice |

Analysis

| Issue | Action |

|---|---|

| INV102 Missing | Follow up with Vendor B |

| INV104 Duplicate | Remove duplicate entry |

| INV105 Unknown | Verify accounting records |

| Remaining invoices | Eligible for ITC |

By identifying these exceptions before filing GSTR-3B, the business avoids incorrect ITC claims and improves compliance.

Best Practices for GST Reconciliation

A disciplined reconciliation process helps businesses reduce compliance risks and improve reporting accuracy.

Reconcile Monthly

Waiting until the end of the financial year makes reconciliation significantly more difficult.

Monthly reconciliation keeps discrepancies manageable and allows timely corrections.

Standardize Invoice Formats

Consistent invoice numbering and formatting improve matching accuracy and reduce false mismatches.

Validate GSTINs

Incorrect GSTINs are among the leading causes of reconciliation issues.

Use GSTIN validation during customer and supplier onboarding.

Maintain Digital Records

Store invoices electronically in a centralized repository.

This simplifies:

- Invoice retrieval

- Audit preparation

- Vendor communication

- Historical reconciliation

Track Vendor Compliance

Develop a vendor scorecard that monitors:

- Timely return filing

- Invoice accuracy

- Frequency of mismatches

- Correction turnaround time

This helps identify suppliers that may delay your ITC claims.

Perform Internal Reviews

Before filing returns:

- Review high-value invoices.

- Verify tax calculations.

- Check amendments.

- Confirm credit and debit notes.

- Ensure all invoices belong to the correct tax period.

Automating GST Reconciliation with BillsDeck

As invoice volumes grow, manual reconciliation becomes increasingly time-consuming and prone to errors. Automation helps finance teams focus on exception handling instead of repetitive data entry.

Challenges of Manual Reconciliation

Manual processes often involve:

- Downloading invoices from emails.

- Entering data into spreadsheets.

- Comparing invoice values line by line.

- Checking GST rates manually.

- Following up with suppliers for missing invoices.

These activities consume valuable time and increase the likelihood of errors.

How BillsDeck Simplifies the Process

BillsDeck helps businesses digitize invoice processing before reconciliation begins.

Key capabilities include:

- AI-powered OCR for PDF invoices, scanned documents, and images.

- Automatic extraction of invoice numbers, GSTINs, dates, taxable values, and GST amounts.

- Standardized invoice data for consistent downstream processing.

- Export to accounting systems in structured formats.

- Reduced manual keying and validation effort.

- Faster invoice processing and improved data accuracy.

By capturing invoice data accurately at the source, finance teams can spend less time correcting errors and more time resolving genuine reconciliation exceptions.

Learn more about invoice automation at https://billsdeck.com.

GST Reconciliation Checklist

Use the following checklist at the end of every GST reporting cycle.

| Task | Completed |

|---|---|

| Sales register updated | □ |

| Purchase register updated | □ |

| Supplier invoices collected | □ |

| Credit notes recorded | □ |

| Debit notes recorded | □ |

| GSTINs validated | □ |

| GSTR-1 reconciled | □ |

| GSTR-2B reconciled | □ |

| GSTR-3B verified | □ |

| ITC reviewed | □ |

| Exceptions resolved | □ |

| Returns filed | □ |

| Supporting documents archived | □ |

Using a standardized checklist promotes consistency and reduces the chance of missing critical reconciliation steps.

Frequently Asked Questions

What is GST reconciliation?

GST reconciliation is the process of comparing accounting records with GST returns and supplier filings to ensure that invoices, tax amounts, and Input Tax Credit are accurate.

Why is GST reconciliation important?

It helps businesses:

- Claim eligible Input Tax Credit.

- Detect errors before filing returns.

- Reduce GST notices.

- Improve financial reporting.

- Maintain statutory compliance.

Which GST returns are used for reconciliation?

The primary returns include:

- GSTR-1

- GSTR-2B

- GSTR-3B

Some businesses may also reconcile additional statements depending on their industry and reporting requirements.

How often should GST reconciliation be performed?

Monthly reconciliation is considered the best practice. It enables businesses to identify discrepancies early and avoid year-end compliance issues.

What are the most common GST reconciliation mismatches?

Common mismatches include:

- Missing invoices

- Duplicate invoices

- Incorrect GSTIN

- Wrong GST rate

- Incorrect taxable value

- Missing credit notes

- Supplier filing delays

- Incorrect reporting period

Can GST reconciliation be automated?

Yes. Businesses can automate invoice capture, data extraction, validation, and matching using intelligent document processing solutions. Automation reduces manual effort, improves data accuracy, and accelerates reconciliation.

How does BillsDeck help with GST reconciliation?

BillsDeck automates the extraction of invoice data from PDFs, scanned documents, and images using AI-powered OCR. Clean, structured invoice data improves the quality of accounting records and supports faster, more accurate GST reconciliation workflows.

Conclusion

GST reconciliation is more than a compliance requirement—it is a critical financial control that protects businesses from incorrect tax filings, denied Input Tax Credit, and costly penalties. By regularly comparing accounting records with GST returns such as GSTR-1, GSTR-2B, and GSTR-3B, businesses can identify discrepancies early, improve the accuracy of financial reporting, and strengthen audit readiness.

While manual reconciliation may be manageable for businesses with a small number of invoices, growing organizations often deal with thousands of transactions each month. In such cases, automating invoice capture and validation significantly reduces manual effort and improves reconciliation efficiency.

Solutions like BillsDeck streamline the first stage of the process by extracting structured data from invoices using AI-powered OCR. When accurate invoice information flows into your accounting system, GST reconciliation becomes faster, more reliable, and easier to manage.

Establishing a consistent monthly reconciliation process, maintaining high-quality financial records, and leveraging automation where appropriate will help businesses remain compliant while reducing administrative overhead and enabling finance teams to focus on strategic activities.