Introduction

The golden rules of accounting form the foundation of recording financial transactions. These rules help ensure that every debit has a corresponding credit and that accounts are recorded correctly.

What are the Golden Rules of Accounting?

The golden rules are basic principles used to record journal entries based on account types.

Types of Accounts

Personal Account

Related to individuals or organizations.

Examples:

- Customer accounts

- Supplier accounts

Real Account

Related to assets.

Examples:

- Cash

- Machinery

- Furniture

Nominal Account

Related to income and expenses.

Examples:

- Salary expense

- Rent income

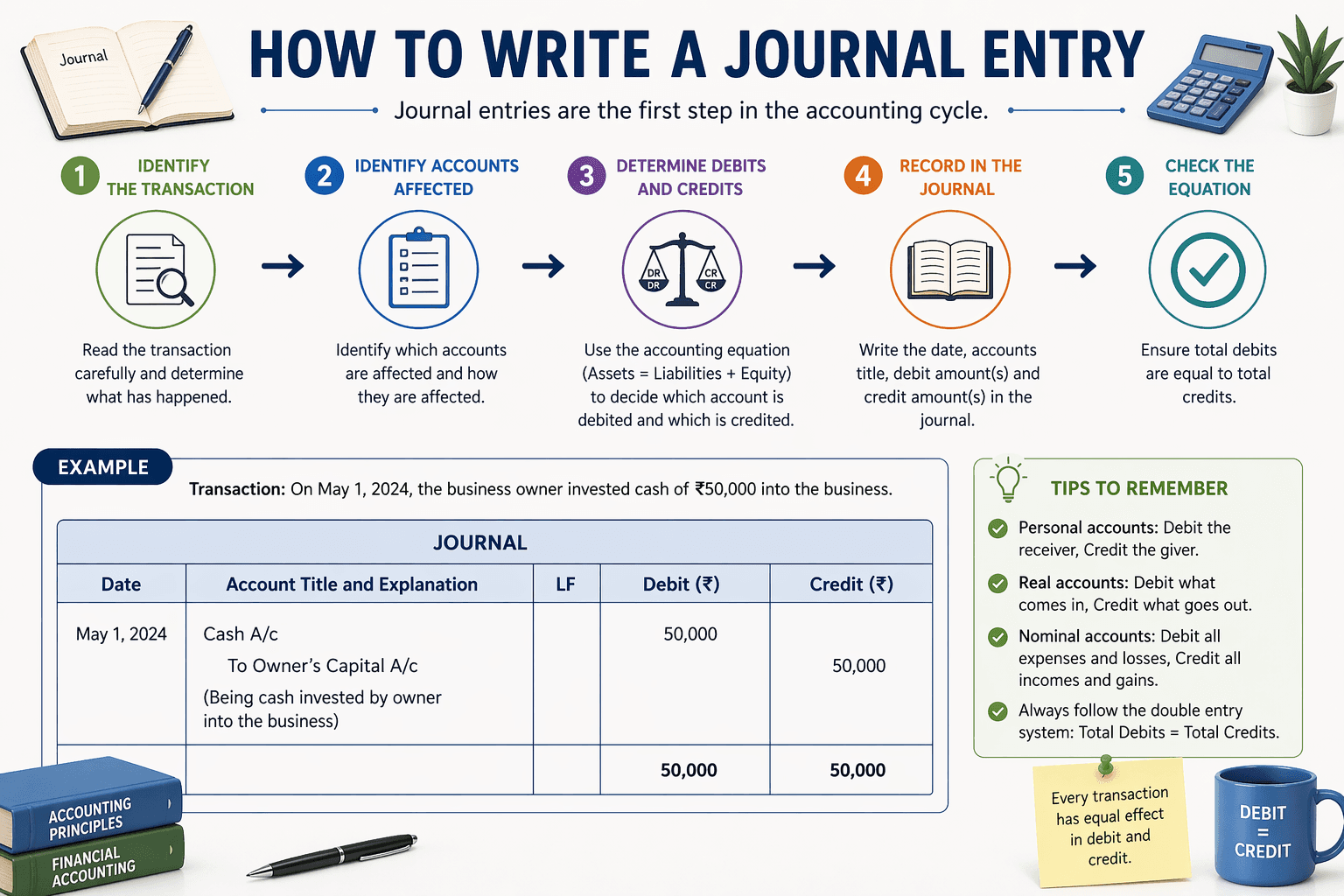

The 3 Golden Rules

-

Personal Account

Debit the receiver, Credit the giver -

Real Account

Debit what comes in, Credit what goes out -

Nominal Account

Debit expenses and losses, Credit income and gains

Golden Rules with Journal Entry Examples

1. Paid rent in cash

- Rent A/c → Debit

- Cash A/c → Credit

2. Purchased furniture for cash

- Furniture A/c → Debit

- Cash A/c → Credit

3. Received cash from customer

- Cash A/c → Debit

- Customer A/c → Credit

Easy Trick to Remember

- Personal → Person

- Real → Things

- Nominal → Expenses & Income

Common Mistakes

- Confusing account types

- Wrong debit/credit entries

- Ignoring transaction nature

Practical Use Cases

- Recording daily transactions

- Preparing financial statements

- Managing business accounts

FAQs

1. Why are golden rules important?

They ensure accurate accounting records.

2. Are these rules still used today?

Yes, even modern accounting systems follow them.

3. Do software tools apply these rules?

Yes, accounting tools automate these rules in the backend.

Conclusion

Understanding the golden rules of accounting makes it easier to record transactions and avoid errors. Whether you’re handling accounts manually or using software, these rules are always at work.

For bulk transaction processing and automated categorization, tools like BillsDeck help apply these rules without manual effort, saving time and reducing errors.